During the week, T-bills recorded an undersubscription, with the overall subscription rate coming in at 94.3% down from the oversubscription of 141.0% recorded the previous week, attributable to the concurrent bond issue. The highest subscription rate was in the 364-day paper of 121.9%, but it was a decline from 190.2% recorded the previous week. Additionally, the Central Bank of Kenya released the auction results for the recently reopened bonds, FXD1/2019/10 and FXD2/2018/20 whose overall subscription rate came in at 97.4%, with the government receiving bids worth Kshs 48.7 bn compared to the Kshs 50.0 bn offered. Standard & Poor’s, lowered its long-term foreign and local currency sovereign credit ratings on Kenya to ‘B’ from ‘B+’ and affirmed the short-term foreign and local currency rating;

Equities

During the week, the equities market recorded mixed performance, with NSE 20 declining by 0.9%, while NASI and NSE 25 gained by 0.3% and 0.9%, respectively, taking their YTD performance to gains of 6.6%, 6.1% and 2.7% for NASI, NSE 25 and NSE 20 respectively. The equities market performance was driven by gains recorded by large-cap stocks such as Equity Group, Diamond Trust Bank (DTB-K) and KCB Group of 5.1%, 4.9%, and 4.6%, respectively. The gains were however weighed down by losses recorded by stocks such as NCBA, Bamburi, and ABSA Bank, which declined by 4.1%, 3.0% and 1.9%, respectively;

Real Estate

During the week, the Kenya Bankers Association (KBA) released the Housing Price Index, March 2021 Report, highlighting that house prices rose by 0.2% in Q4’2020, an improvement from the 0.1% contraction recorded in Q3’2020. In the residential sector, Sycamore Pine Limited, a real estate developer announced plans to construct 1,959 residential apartments under a project dubbed Samara Estate to be located in Migaa Gold Estate in Kiambu County;

Focus of the Week

Financial planning for education is the practice and habit of managing one’s finances with the intention of saving towards the funding of their children’s’ education in the future. This week, we follow up on our previous focus on Education Investment Plans in Kenya by bringing on the financial planning aspect of it, the available options and the considerations to make when choosing the best investment avenue for education;

Fixed Income

Money Markets, T-Bills & T-Bonds Primary Auction:

During the week, T-bills recorded an undersubscription, with the overall subscription rate coming in at 94.3% down from 141.0% recorded the previous week, attributable to the concurrent bond issue coupled with the tightened liquidity in the money markets. The highest subscription rate was in the 364-day paper, which declined to 121.9% from 190.2% recorded the previous week. The subscription rate for the 91-day and 182-day papers also declined to 108.8% and 60.8%, from 176.1% and 77.7% recorded the previous week, respectively. The yield on the 91-day paper remained unchanged at 7.0%, while the yields on 364-day and 182-day papers rose by 7.3 bps and 6.7 bps to 9.1% and 7.8%, respectively. The government accepted 100.0% of bids received, amounting to Kshs 22.6 bn.

On the Primary Bond Market, there was an undersubscription for this month’s bond offers, with the overall subscription rate coming in at 97.4%, attributable to the relatively tight but recovering money market liquidity. The Central Bank of Kenya had re-opened 2 bonds, FXD1/2019/10 and FXD2/2018/20 with effective tenors of 8.0 and 17.4 years, and coupons of 12.4% and 13.2%, respectively, in a bid to raise Kshs 50.0 bn for budgetary support. The government received bids worth Kshs 48.7 bn, and accepted only Kshs 48.3 bn, translating to an acceptance rate of 99.2%. Investors preferred the 20-year bond issue i.e. FXD2/2018/20, which received bids worth Kshs 32.8 bn, representing 65.6% of the total bids received. The weighted average rate of accepted bids for the two bonds came in at 12.4% and 13.4%, for FXD1/2019/10 and FXD2/2018/20, respectively.

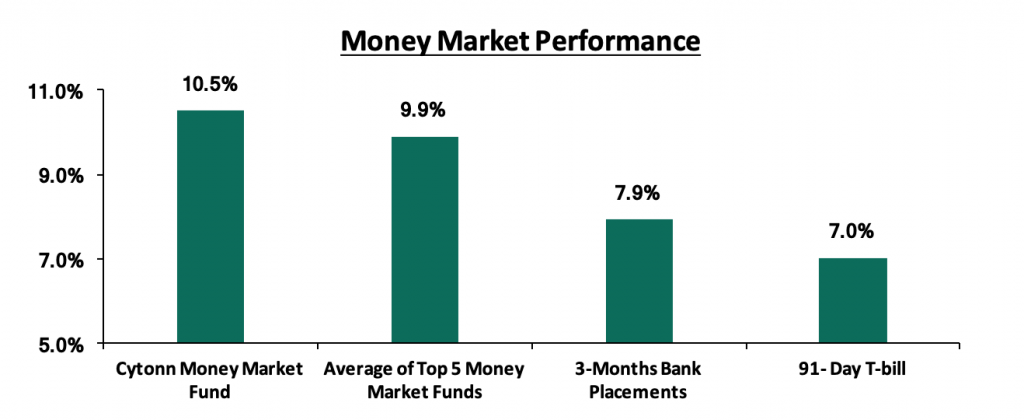

In the money markets, 3-month bank placements ended the week at 7.9% (based on what we have been offered by various banks), while the yield on the 91-day T-bill remained unchanged at 7.0%, same as recorded last week. The average yield of the Top 5 Money Market Funds declined marginally by 0.1% points to come in at 9.9%, from 10.0% recorded last week. The yield on the Cytonn Money Market also declined during the week by 0.4% points to come in at 10.5%, from 10.9% recorded the previous week.

Liquidity:

During the week, liquidity in the money market tightened, with the average interbank rate increasing marginally by 0.1% points to 5.0%, from the 4.9% recorded the previous week, attributable to the government payments which were partly offset by tax remittances. The average interbank volumes increased by 12.6% to Kshs 13.0 bn, from Kshs 11.6 bn recorded the previous week. According to the Central Bank of Kenya’s weekly bulletin released on 12th March 2021, commercial banks’ excess reserves came in at Kshs 11.7 bn in relation to the 4.25% Cash Reserve Ratio.

Eurobonds performance:

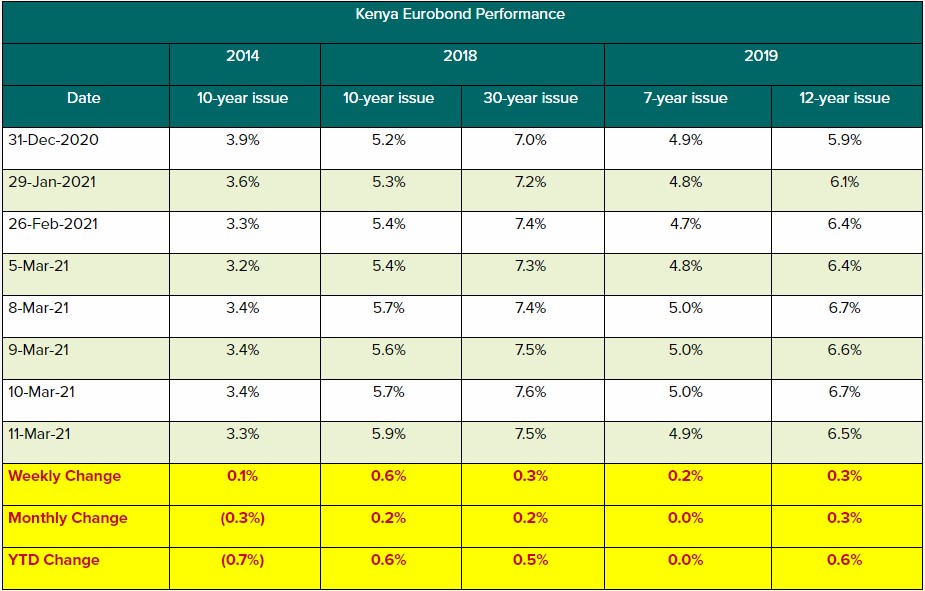

During the week, the yields on Eurobonds were on an upward trajectory. According to the Central Bank bulletin, the yields on the 10-year Eurobond issued in June 2014, the 10-year and 30-year Eurobonds issued in 2018 and the 7-year and 12-year Eurobonds issued in 2019 all increased by 0.1%, 0.6%, 0.3%, 0.2% and 0.3% points to 3.3%, 5.9%, 7.5%, 4.9% and 6.5% respectively, from 3.2%, 5.3%, 7.3%, 4.6% and 6.3%.

Kenya Shilling:

During the week, the Kenyan shilling appreciated marginally by 0.03% against the US dollar to Kshs 109.6, from Kshs 109.7 recorded the previous week. This was mainly attributable to market participants anticipating a positive economic recovery following the arrival of the Covid-19 vaccine in the country. On a YTD basis, the shilling has depreciated by 0.4% against the dollar, in comparison to the 7.7% depreciation recorded in 2020. We expect continued pressure on the Kenyan shilling due to:

- A slowdown in foreign dollar currency inflows due to reduced dollar inflows from sectors such as tourism and horticulture, and,

- Continued uncertainty globally making people prefer holding dollars and other hard currencies.

However, in the short term, the shilling is expected to be supported by:

- The Forex reserves which are currently at USD 7.4 bn (equivalent to 4.5-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover. The Forex reserves have been declining and are now at the same level as the EAC criteria for import cover. Countries use foreign currency reserves to keep a fixed or quasi-fixed rate value, maintain competitively priced exports, remain liquid in case of crisis, and provide confidence for investors. Therefore, the dwindling in the forex reserves may mean the government of Kenya will struggle to support the local currency when it depreciates,

- The improving current account position which narrowed to 4.8% of GDP in the 12 months to December 2020 compared to 5.8% of GDP during a similar period in 2019, and,

- Improving diaspora remittances evidenced by a 19.7% y/y increase to USD 299.6 mn in December 2020, from USD 250.3 mn recorded over the same period in 2019, has cushioned the shilling against further depreciation

Weekly Highlight:

During the week, Standard & Poor’s, a US-based credit rating agency, lowered its long-term foreign and local currency sovereign credit ratings on Kenya to ‘B’ from ‘B+’, on the back of the effects of the ongoing pandemic which resulted in GDP contraction of 5.7% and 1.1% in Q2’ and Q3’2020, respectively, and increasing debt levels, which in turn increase the country’s vulnerability to debt defaults.

Kenyan Business Feed is the top Kenyan Business Blog. We share news from Kenya and across the region. To contact us with any alert, please email us to [email protected]

{kind=link}